Are you involved in a dispute over the validity of a Will?

You need an experienced attorney specializing in contested wills!

Are you involved in a gift that is being contested?

You need an experienced attorney specializing in contested gifts!

Are you involved in a guardianship matter?

You need an experienced and caring guardianship attorney!

Are you involved in a dispute over an Estate or Trust accounting?

You need an experienced and caring litigation attorney!

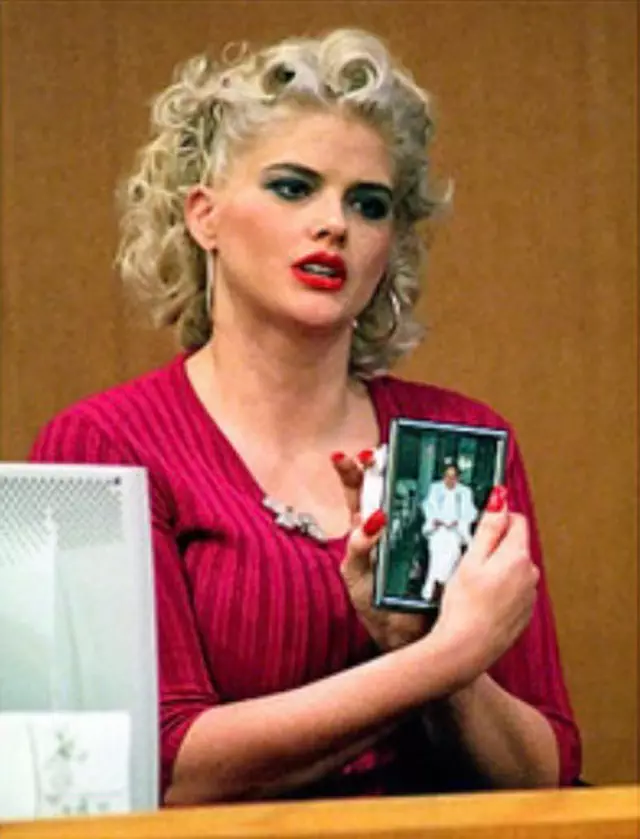

Listen to the news, read the newspaper, or surf the web and you can’t help but hear about famous estate litigation cases. Whether it’s determining who the guardian should be for Michael Jackson’s children, how much of the Leona Helmsley estate should pass to her dog, Trouble, or whether or not Anthony Marshall unduly influenced his philanthropic mother, Brooke Astor to change her Will in his favor, one thing is for sure – such contested estates aren’t unique to rock stars or land barons, but rather, affect hard working families day in and day out.

- Claims of undue influence;

- Lack of capacity;

- Change in the titling of assets either by a power of attorney or an heir altering the dispositive intent of the testator;

- Demands for an estate accounting and objections to the accounting when produced;

- Removal of an executor; or

- Actions challenging trustees as to the investment management of a trust portfolio;

Surrogate Court dockets are filled with cases involving family members fighting over the assets and intentions of a deceased parent or spouse. Each case is different and the laws vary from state to state. Accordingly, this website is intended to provide the browser with general, current, interactive information written by an attorney whose practice is geared towards probate litigation and contested estates.

Russell J. Fishkind, Esq. has been assisting his clients to successfully resolve estate disputes for over 30 years. He’s a Partner with the law firm Saul Ewing, LLP, an Associate Adjunct Professor at New York University, the author of Probate Wars of the Rich and Famous – An Insider’s Guide to Estate Planning and Probate Litigation, and the co-author of JK Lasser’s Estate & Business Succession Planning. Mr. Fishkind brings years of both courtroom experience and practical advice into his educational Estate Litigation Video series to help browsers better understand this unique area of the law.

Russell is joined by Ronald P. Colicchio, Esq., who is a graduate of New York University School of Law where he earned both his law degree and a Masters in Taxation. Ronald is admitted to practice law in the states of New York, New Jersey and Florida, and has represented clients in estate and trust matters for over 27 years. Together, their estate and trust litigation practice focuses on the representation of individuals and corporate fiduciaries in matters involving allegations of undue influence, fraud or lack of capacity, Will contests, contested inter vivos transfers, changes of beneficiaries on accounts, contested accountings, actions for breach of fiduciary duty, contested guardianships, Power of Attorney actions, forgeries, and other contested trust and estate matters.

The Probate Litigation New Jersey Resource Center is designed to be educational. Should you have a question, you can email or call Russell J. Fishkind, Esq. or Ronald P. Colicchio, Esq. for a response.

Should you be interested in reading more about both estate planning and estate litigation, Mr. Fishkind recently authored Probate Wars of the Rich & Famous: An Insider’s Guide to Estate Planning and Probate Litigation, which tracks the estate battles of Anna Nicole Smith, Brooke Astor, Michael Jackson, Nina Wang, Jerry Garcia and Leona Helmsley and identifies the five universal factors that caused such disputes. Each chapter provides estate planning insights designed to help individuals plan their estates without causing litigation. If, however, probate litigation cannot be avoided, the book also provides invaluable lessons about undue influence claims, how to remove a fiduciary, demanding an estate accounting and filing claims seeking to set aside lifetime transfers that undermined the decedent’s intentions. Few, if any, estate planning books utilize colorful celebrity accounts to provide meaningful insights and actionable advice.